Capital gains on home sale is something every homeowner worries about when selling. You’ve built memories in the house, made upgrades, and now you want the money you earn to stay in your pocket, not get eaten up by taxes. The reality is, without planning, selling your home can have some unpleasant tax consequences of selling a home. But the good news? There are ways to reduce, or even avoid, capital gains tax on home sales, and it’s easier than most people think.

What Are Capital Gains on Home Sale?

Here’s the deal. When you sell your home for more than you paid, the difference is a capital gain. That’s the amount the government can tax. But here’s where it gets better: not every dollar of gain is taxable. How much you owe depends on:

- How long you’ve owned the home – short-term gains (less than a year) get taxed at regular income rates, long-term gains (over a year) get better rates.

- Whether it’s your main home – if it is, the primary residence capital gains exclusion can save you a ton.

- What you spent improving the property – those renovations can bump up your home’s basis, reducing taxable gain.

Basically, knowing the rules can save you thousands when it comes to tax on selling property.

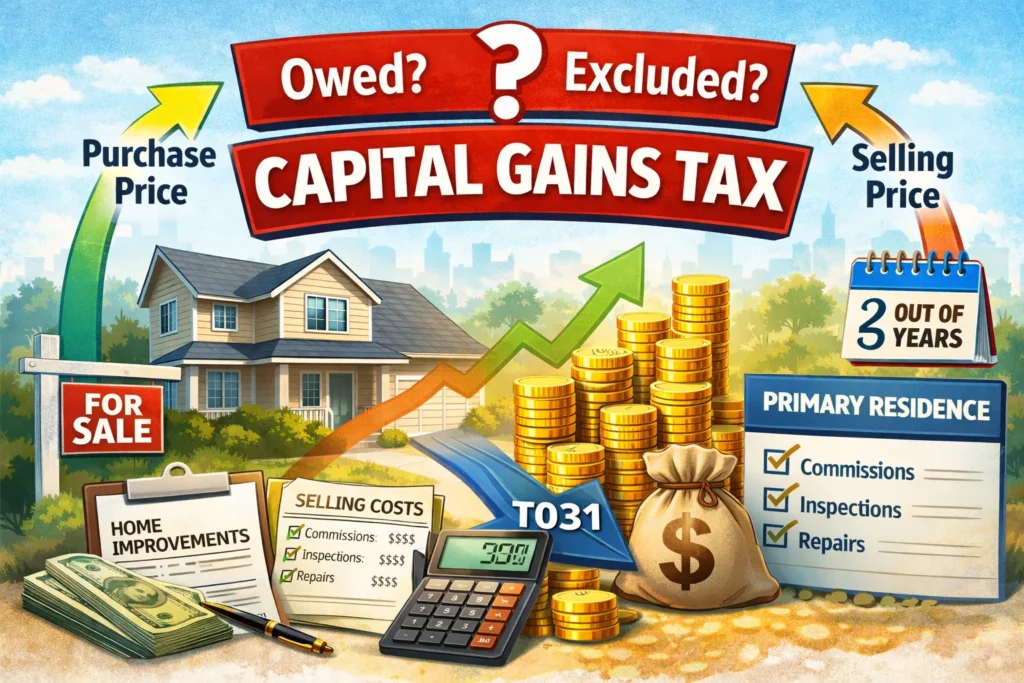

How the Tax on Selling House Works

Most homeowners think selling a home is just about listing it at the right price. Nope. The selling house tax implications can change your take-home money dramatically. Here’s a simple breakdown:

- Cost basis matters – That’s what you originally paid for the house plus any improvements you made. The higher it is, the less you owe in taxes.

- Primary residence exclusion – If you lived in the house 2 out of the last 5 years, you can exclude up to $250,000 (single) or $500,000 (married) from taxes.

- Selling costs count – Commissions, legal fees, inspections, and even some repairs before selling can lower your taxable gain.

Here’s a quick table to make it visual:

| Factor | How It Affects Your Tax |

| Purchase Price | Starting point for gain calculation |

| Selling Price | Determines your total profit |

| Home Improvements | Increase basis, reduce taxable gain |

| Selling Costs | Lower net gain subject to tax |

How to Reduce Capital Gain Tax Without Tricks

Nobody likes paying more than they need to. Here’s what can really help:

- Use your primary residence exclusion

Live in your home 2 out of the last 5 years? Boom – up to $250k/$500k can be excluded. That’s potentially huge. - Time your sale

If you’re not quite at the 2-year mark, waiting a few months could save a lot. - Offset gains with losses elsewhere

Sold some losing investments? That loss can offset the gain from your home sale. - Deduct your selling expenses

Commissions, inspections, repairs, legal fees – they all count. Keep your receipts. - 1031 exchange for investment properties

Only for rentals or investment homes, but it lets you defer taxes by reinvesting in another property.

Real-Life Example

Let’s make this concrete. Say you bought a home for $400,000, made $50,000 in renovations, and sold it for $700,000. Selling costs were $30,000.

| Details | Numbers |

| Purchase Price | $400,000 |

| Selling Price | $700,000 |

| Home Improvements | $50,000 |

| Selling Costs | $30,000 |

| Adjusted Gain | $220,000 |

| Exclusion Applied | $220,000 |

| Taxable Gain | $0 |

Because of the primary residence capital gains exclusion, this homeowner doesn’t owe a dime. Money stays where it belongs – in their hands.

Common Mistakes That Cost Money

Here’s what trips people up:

- Assuming all gains are taxable – Exclusions exist, and they’re significant.

- Ignoring home improvements – Those receipts for renovations are gold for reducing capital gains on home sale.

- Selling multiple properties in a single year without planning – You could bump yourself into a higher tax bracket if you’re not careful.

Step-by-Step Plan Before Selling

Think of this like a roadmap:

- Calculate your potential gain – Know the purchase price, selling price, and improvements.

- Check if you qualify for the exclusion – Did you live in the house 2 out of the last 5 years?

- Time your sale – Sometimes waiting a few months can make a huge difference.

- Keep all records – Every renovation, repair, or cost can reduce taxable gain.

- Talk to a tax professional – Rules change, and professionals help you make sure nothing slips through the cracks.

How to Avoid Capital Gains Tax on Real Estate

You can’t always escape taxes, but you can reduce them:

- Reinvest in another primary home.

- Use installment sales to spread the gain over years.

- Offset gains with investment losses.

Seniors and Selling Homes

If you’re 55 or older, check for extra perks in your state:

- One-time exemptions may apply on top of federal rules.

- Downsizing could trigger additional benefits.

Conclusion:

Capital gains on home sale doesn’t have to eat your profits. Plan ahead, track improvements, and know your exclusions. Using a tax professional can save a lot more than their fee.

Frequently Asked Questions

What is the maximum exclusion for a primary residence?

You can exclude up to $250,000 for single owners or $500,000 for married couples if you lived in the house 2 of the last 5 years.

Do renovations reduce taxable gain?

Yes. Home improvements increase your basis, lowering your capital gains on home sale.

How long do I need to live in the home?

2 out of the last 5 years. That’s it.

Are selling costs deductible?

Yes, things like agent commissions, inspections, and legal fees count.

Can I defer taxes with a 1031 exchange?

Yes, but only for investment properties, not your primary home.

Does selling a rental home count for the same exclusion?

No. Only primary residences qualify. Rental or investment homes follow different rules.

Can losses elsewhere reduce my gain?

Absolutely. Capital losses from other investments can offset home gains.

Do frequent moves affect the exclusion?

Yes, if you don’t meet the 2-year residency rule within the last 5 years.

Will I owe state taxes?

Some states have their own rules. Check local laws.

What if I sell at a loss?

Losses on a primary home aren’t deductible, but investment property losses may help offset gains elsewhere.