Let’s talk about something that confuses a lot of people but can actually save you a ton of money: the state and local tax deduction. If you pay state income tax, property tax, or even sales tax, this is your chance to reduce your federal tax bill. And in 2026, understanding it is more important than ever because of the salt deduction cap.

Here’s the deal: a lot of people don’t even realize how much of their taxes they can actually deduct. That’s where knowing about salt tax, salt deductions explained, and smart planning comes in. This isn’t complicated if you know what to do. Let’s break it down.

What Is SALT Anyway?

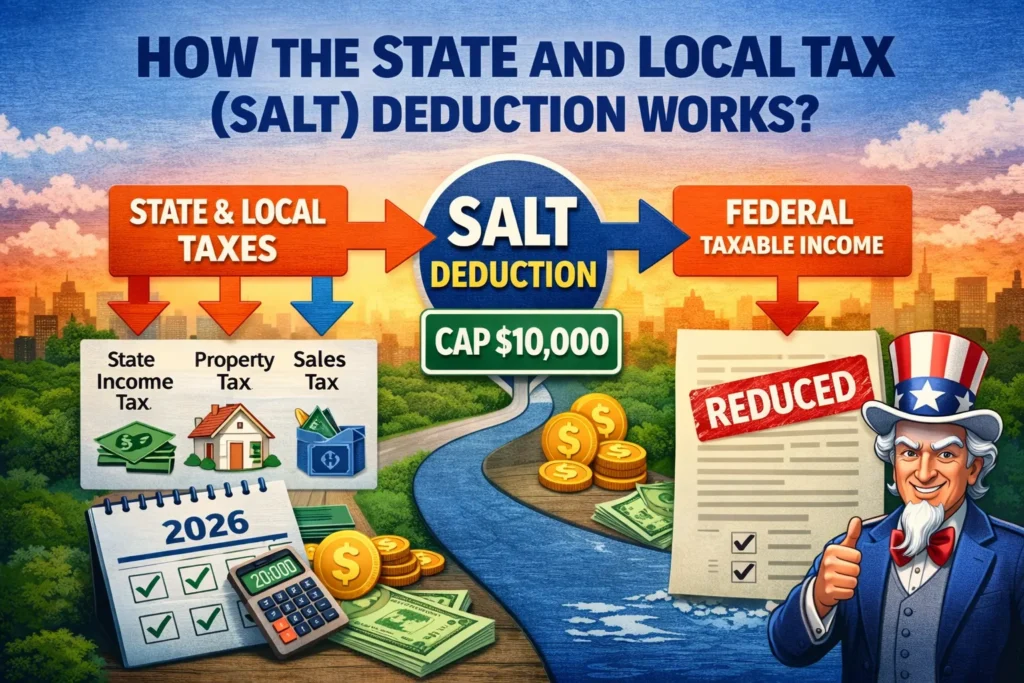

SALT stands for state and local taxes. That’s basically any tax you pay to your state or local government—your income taxes, property taxes, and yes, even sales taxes if you pick that option.

Here’s the thing about the state and local tax deduction: it lets you subtract these taxes from your federal taxable income. Sounds great, right? But there’s a catch—the salt deduction cap. Even if you pay $20,000 in state and local taxes, you can only deduct $10,000. That’s the limit for individuals and married couples filing jointly.

Think of it like a ceiling. Anything above that? You don’t get to write it off.

| Tax Type | Can You Deduct It? | Notes |

| State Income Tax | Yes | Included in the $10,000 cap |

| Local Income Tax | Yes | Covers cities, towns, municipalities |

| Property Tax | Yes | Paid on your home, counts toward cap |

| Sales Tax | Optional | Pick this if it saves you more than income tax |

How This Actually Works in 2026

Here’s the real-life version of what the state and local tax deduction does for you: it lowers your federal taxable income if you itemize your deductions. That means if you take the standard deduction, sorry—you’re out of luck for SALT.

Some things to remember:

- Income and property taxes are the main players here.

- In low or no-income-tax states, the state sales tax deduction can actually give you a bigger break.

- Tools like a salt tax calculator can help figure out whether you’re better off itemizing or taking the standard deduction.

Smart Moves to Maximize Your SALT Deduction

You can’t control the salt deduction cap, but you can control how you play your taxes. Here’s how:

- Prepay property taxes: Pay December’s taxes for next year, and boom—you can include them in the current year’s deductions.

- Track sales tax carefully: If your state doesn’t have income tax, deducting sales tax could save more.

- Bunch your payments: Got multiple big tax bills? Combine them in one year to maximize your deductions for state and local taxes.

- Plan around one-time bills: Big property assessments or special taxes? Strategize when to pay them to get the most deduction.

Why High-Tax States Need This

If you live in a state with high income or property taxes, the salt tax can be huge. That’s why knowing the state and local tax deduction rules is critical. Planning is everything here because hitting the salt deduction cap means leaving money on the table if you’re not careful.

Homeowners, Listen Up

Property taxes are usually the biggest chunk of your SALT deduction. Keep receipts, track payments, and figure out whether the state sales tax deduction might actually be a better choice. This is how homeowners get real savings.

Small Business Tips

Small business owners pay state and local taxes, too. Deducting them properly reduces taxable income. Professional guidance can make sure you’re not missing anything.

Staying Under the SALT Deduction Cap

Even with smart moves, you can’t beat the $10,000 limit. But:

- Spread payments if possible, or prepay strategically.

- Combine with other deductions like charitable contributions to lower your overall taxable income.

Common Mistakes People Make

- Thinking it’s unlimited. Nope. The salt deduction cap is real.

- Assuming only income tax counts. Property and sales taxes can count too.

- Believing everyone benefits the same. Low-tax states won’t see much from SALT.

Tools That Make Life Easier

- SALT Tax Calculator: See how much you can deduct before you file.

- Tax Software: Most programs automatically calculate your state and local tax deduction.

- Tax Advisors: Especially helpful if you’re in a high-tax state or have a big home.

Conclusion:

The state and local tax deduction is still a solid way to save money on federal taxes.

Planning payments and keeping records maximizes your deductions for state and local taxes. Choosing state sales tax deduction instead of income tax might increase savings in some states.

Frequently Asked Questions

What is the SALT deduction?

It’s a way to subtract state and local taxes, like income, property, or sales taxes, from your federal taxable income if you itemize.

How much can I deduct with the SALT cap?

The salt deduction cap limits your deductions to $10,000 per year, regardless of how much you actually pay.

Can I pick sales tax instead of income tax?

Yes. The state sales tax deduction can sometimes give you a bigger break, especially in states with low or no income tax.

Are property taxes included?

Absolutely. Property taxes count toward your deductions for state and local taxes, but remember the $10,000 cap.

How does it affect high-tax states?

High-tax states pay more, so the salt tax is bigger, but the salt deduction cap still limits how much you can deduct.

Does prepaying taxes help?

Yes. Prepaying property or other taxes lets you maximize the state and local tax deduction in a single year.

Can small businesses use SALT?

Yes. Businesses paying state and local taxes can reduce taxable income, but planning is crucial.

Does the standard deduction include SALT?

No. Only itemized deductions allow a state and local tax deduction.

What tools help calculate SALT?

A salt tax calculator, tax software, or professional advice can show your best deduction strategy.

Can the SALT cap be legally bypassed?

Not directly. But prepayments, bunching, and pairing with charitable deductions can optimize benefits within the deductions for state and local taxes.