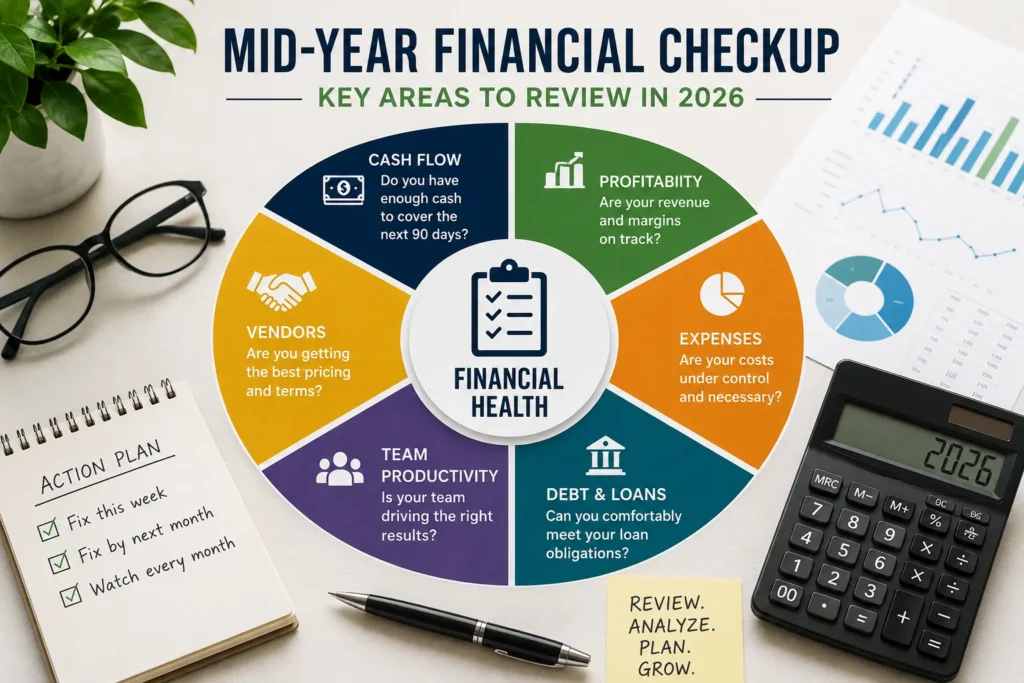

A financial checkup is something most business owners avoid until December. Then they panic. Do not be that person. Mid-year is your sweet spot. You have five months of real data. You have six months left to fix things. Let us walk through exactly the financial health checklist.

Why Bother With a Financial Check Up Now?

Waiting until year-end is like driving with your eyes closed. You might be fine. You might crash. A financial check up in July tells you if you are speeding toward a wall. If sales are down, you still have time to market harder. If costs are up, you can cut before they kill you. If taxes are going to hurt, you can set money aside now. Do this and you sleep better in the fall.

Grab These Three Papers First

You cannot review what you cannot see. Get these financial assessment:

- Profit and Loss for January through May

- Balance Sheet for end of May

- Cash Flow Statement for same period

If your books are a mess, hire professional bookkeeping services. A good bookkeeper costs less than one bad business decision. Trust me on that.

Check Your Quick Cash Situation

Here is a simple test. Add up cash in the bank, money customers owe you, and anything you can sell fast. That is your liquid assets. Now add up every bill due in the next 90 days. Rent. Payroll. Suppliers. Loans. Taxes. Divide assets by bills.

If the number is below 1.2, you are tight. Below 1.0, you have a problem. Do not panic. You just need to collect faster or push some bills out. But you have to know the number first. That is the whole point of a financial health check.

Compare Real Numbers to Your Wishful Thinking Budget

Your budget from January is probably wrong. That is fine. But you need to see where you missed. Look at revenue first. Are you actually making what you thought? If not, is that a one-month blip or a three-month trend? Trends require action. Blips do not.

Now look at your biggest expenses. Pick the top three that are over budget. Ask yourself: do I really need to spend this much? Often the answer is no. You just got lazy. A financial health assessment exposes lazy spending.

Your Gross Margin Tells the Real Story

Gross margin is what you keep after paying for materials and direct labor. If you sell something for 100 dollars and it costs you 40 dollars to make, your gross margin is 60 percent. Simple.

Calculate yours for each month of 2026. Now compared your financial check up to last year. If your margin dropped by more than 5 percent, you have a pricing problem or a supplier problem. Fix this before chasing more sales. Selling more at a bad margin just makes you lose more money faster. A business financial review always starts here.

Can You Actually Pay Your Loans?

Here is a number banks love. Take your monthly profit before interest and taxes. Divide it by your monthly loan payments. That is your debt service ratio.

If the result is below 1.0, you are not earning enough to pay your debts. You are digging a hole. Above 1.25 is safe. Above 1.5 is strong. If you are below 1.2, you have three moves:

- Cut expenses to free up cash

- Refinance to lower your payment

- Sell something you do not need

Do not ignore this. It does not get better on its own.

What Will Your Bank Account Look Like in 90 Days?

Past numbers are history. Cash flow is about tomorrow. Take your average monthly income from the last three months. Subtract your average monthly bills. Now add any big expenses coming up. Insurance. Property taxes. Annual software fees. Big inventory buys.

Does your cash go negative in any month? If yes, act now. Ask customers to pay deposits. Ask vendors for longer terms. Delay buying that new laptop. Draw a line of credit before you are desperate. Banks lend when you do not look desperate for financial check up.

Are Your Vendors Quietly Overcharging You?

Most vendors raise prices every year. Most business owners never notice. Pick your top five vendors by how much you pay them. Call each one. Ask two questions:

1. Can I have a discount for paying on time?

2. Is this your best price or should I check with your competitor?

You will be shocked how often they say yes. A 3 percent discount from five vendors is free money. This takes one hour. Do it.

Is Your Team Productive Enough?

Labor is your biggest cost. But do not just look at payroll. Look at what you get for it. Divide your total revenue by the number of employees. That is revenue per person. Compared to other businesses like yours for financial check up. If you are way below average, you have two choices:

- Sell more without hiring more people

- Hire fewer people

The first choice is better. Better training. Better tools. Better processes. But if you have people doing nothing, you know what to do. A small business financial health review is honest about hard choices.

Write Your Three Lists

A financial check up without action is a waste of time. Write three lists.

- Fix this week: Things that hurt cash flow right now. Example: call every customer who is 60 days late.

- Fix by the end of next month: Things that need planning. Example: call vendors to renegotiate prices.

- Watch every month: Things that can drift. Example: your gross margin percentage.

Put deadlines on your calendar. Do the work. Then do another financial check up in December. You will thank yourself.

Frequently Asked Questions

How often should I really do a financial check up?

Every quarter for a quick look. A full financial health assessment twice a year. Mid-year and year-end. That is plenty.

Can I do a financial check up myself without hiring anyone?

Yes, if your business is small. Under 50 transactions a month, use a spreadsheet. Over that, get software or a bookkeeper. Your time is worth more than data entry.

How long does a mid-year financial check up take?

Three to four hours for most small businesses. One full day if you are bigger. The second time you do it, it goes faster.

What if I find something really bad?

Do not panic. Fix cash flow first. Then fix profit. Then fix debt. Talk to someone you trust. One problem at a time.

What is the number one mistake people make in financial check up?

They look at profit but ignore cash flow. You can be profitable and still go broke because you ran out of cash. Always check both.

When should I hire professional bookkeeping services?

When you spend more than five hours a month on books. Or when you dread opening your accounting software. Or when the IRS sends you a letter. Any of those is a sign.

What is a healthy cash ratio for a small business?

Between 1.5 and 3.0. Below that, you are tight. Above that, you have too much cash sitting around not working for you.

How do I know if my margin is good enough for financial check up?

Compared to your industry. A software company might keep 80 percent. A restaurant might keep 30 percent. If you do not know your industry number, your margin should cover all your bills plus leave 10 percent for profit.

What if I have no budget to compare against?

Then make a simple one now. Take last year’s numbers. Add 5 percent for growth. Subtract 3 percent for efficiency. That is your budget. It is better than nothing.

Is 2026 special compared to other years for financial check up?

Yes. Prices have settled but they are higher than before. Your 2019 margins are gone. Compare yourself to 2025. That is your real baseline. A business financial review in 2026 needs honest comparisons.